ITOCHU: Hedging inflation risks with real assets

By prioritizing capital efficiency and deepening its footprint in the domestic consumer sector, ITOCHU is attempting to pivot downstream and grow its non-resource business sectors.

As Japan navigates a complex macroeconomic landscape defined by geopolitical tensions and a historic shift in monetary policy, the nation’s leading trading houses, also known as Sogo-Shosha, have emerged as the bedrock of a reinvigorated economy. Among these, ITOCHU stands out for its strategic pivot toward downstream consumer industries and superior capital efficiency.

When it comes to geopolitics, Japan is navigating a narrow policy path. Balancing US-China relations alongside inflationary pressures and yen volatility, the country is executing one of the broadest economic reforms in decades. While "Abenomics" initially transformed the direction of both monetary and fiscal policies, the current environment marked by an inflation-conscious Bank of Japan and a government balancing economic growth with fiscal discipline continues to shape the structural evolution of the Japanese economy.

Despite these shifting administrations, the role of the Sogo-Shosha remains a consistent pillar of economic stability. These sprawling, diversified conglomerates, ranging from natural resources to global consumer brands, historically maintained a relatively low profile. However, this somewhat changed when Berkshire Hathaway announced their acquisition of multi-billion-dollar stakes in Mitsubishi Corp, Sumitomo Corp, ITOCHU Corp, Mitsui & Co, and Marubeni Corp, signaling a Buffett vote of confidence in the sector’s value proposition.

Amidst the flurry of investor-friendly corporate reforms, ITOCHU distinguishes itself through a rigorous focus on shareholder returns and capital efficiency. This discipline ensures that ITOCHU maintains one of the highest return on equity profiles across the trading houses.

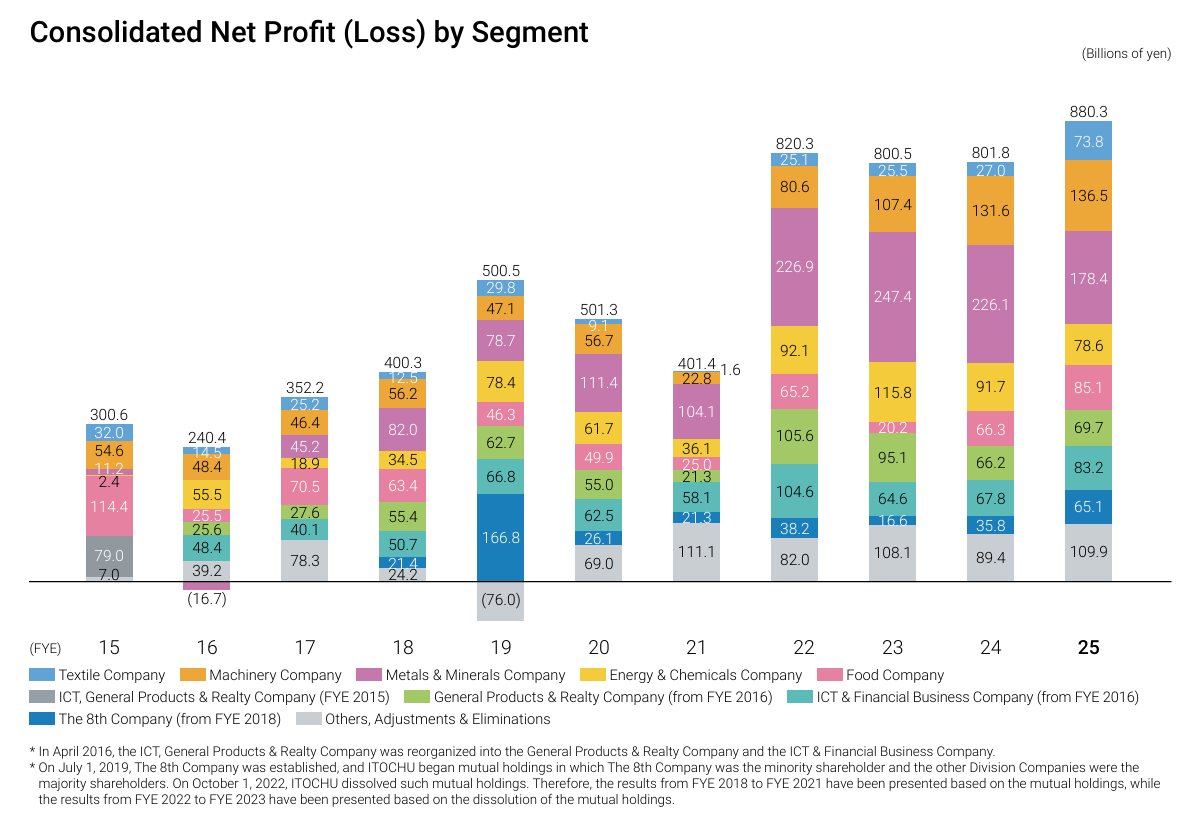

Among the three largest by net income (namely Mitsubishi, Mitsui & Co, and ITOCHU), Mitsubishi is most exposed to upstream businesses due to its significant footprint in the resources industry. Energy, metals and minerals made up almost half of Mitsubishi’s Group income, while ITOCHU is more dominant downstream with its resources business only adding up to about one-fifth of their net income. This reduced reliance on asset-heavy resources business is a key reason for ITOCHU to achieve less volatile margins over economic and commodity cycles.

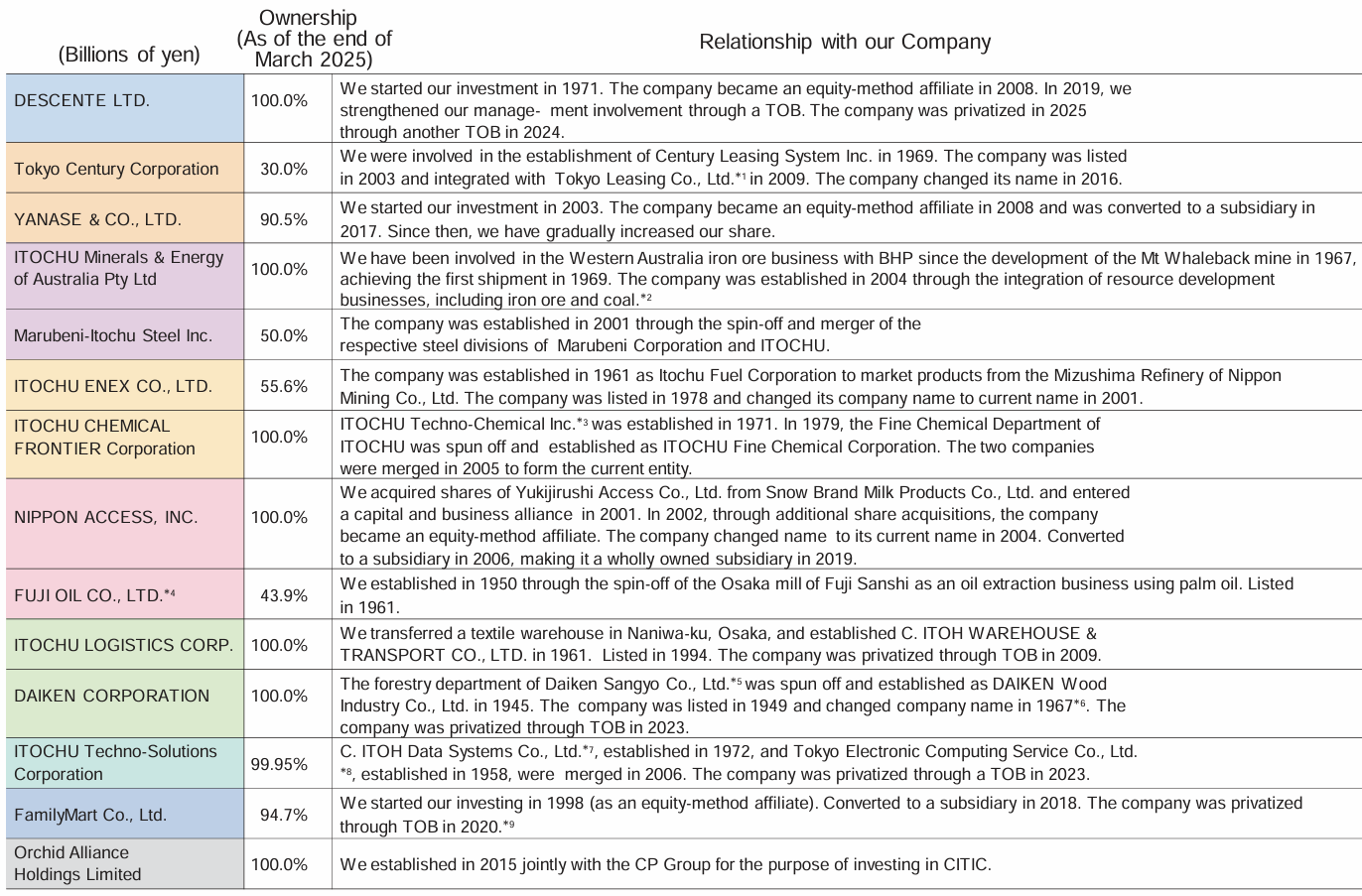

As natural resources become a matter of strategic national interest and supply chain security tightens, B2B operations face an increasingly challenging outlook due to protectionist trade policies. Owning one of the most recognised portfolio of consumer businesses in Japan (such as FamilyMart, DESCENTE, Fuji Oil, HOKEN NO MADOGUCHI, and Nippon-Rent-A-Car), ITOCHU has mitigated these external uncertainties by intensifying its focus on the Japanese domestic market.

ITOCHU management has embarked on increasing stakes in their subsidiaries on multiple occasions. This allowed them to share in a higher proportion of profits while also having more control over the various businesses. This is evident in the string of tender offers in the capital markets, from FamilyMart in 2020 to CTC in 2023 and the latest major transaction being DESCENTE in 2025.

The attempted involvement of the company in the buyout of Seven & i last year further cemented the resolution of ITOCHU in expanding into the consumer and downstream industries of Japan. Even though the bid was eventually withdrawn, ITOCHU managed to pursue an approximately JPY50b investment into Seven Bank, further converting it to an equity-accounted affiliate in December 2025.

It will not be surprising to expect ITOCHU to continue its capital expenditure plans. With a 10% profit growth being a key tenet of the company’s financial matrix, it is essential for new investments and asset replacement to be executed in a timely yet prudent manner. At the same time, by prioritizing capital efficiency and deepening its footprint in the domestic consumer sector, ITOCHU is attempting to further decouple its business growth from the volatility of global commodity cycles.

As Japan makes a gradual but sustained comeback, it is likely that a healthy mix of wages-led inflation and corporate reinvestments will reinvigorate the economy and shake off the shackles of its ‘lost decades’. Largely aligned with government policies under Prime Minister Takaichi, ITOCHU looks primed to ride on this national growth, especially through their FamilyMart and CTC divisions.