Mapletree Pan Asia Commercial Trust: Overseas expansion may not always be the right answer

Beyond the urgency to return to its Singapore-centric focus, a mistiming of capital recycling may risk further valuation derating which can take years to recover.

The performance of Mapletree Pan Asia Commercial Trust (“MPACT”) is one which has to be assessed through a merger lens. In 2022, Mapletree Commercial Trust (comprised of Singapore assets) merged with Mapletree North Asia Commercial Trust (comprised of overseas assets) in a S$4 billion Trust Scheme of Arrangement.

At that time, markets had pushed back on the valuation of Mapletree North Asia Commercial Trust and the lack of an all-cash option for the selling unitholders who may not have wished to continue their investment in the combined entity. The cash-only consideration was subsequently added to the revised terms a few months after the initial announcement, although the valuation remained at 1.0x price-to-book for Mapletree North Asia Commercial Trust’s shares.

What resulted from the merger was a significant change in the overall profile of the merged REIT, comprising both stabilised mature assets in Singapore as well as a handful of commercial assets in gateway Asian cities. The rationale for the merger was clear: A much larger competitive scale and portfolio diversification geographically.

However, in the following years, interest rate hikes globally and weakening fundamentals in most of these gateway markets in North Asia led to challenges for MPACT, which was managing around S$17 billion of assets under management post merger.

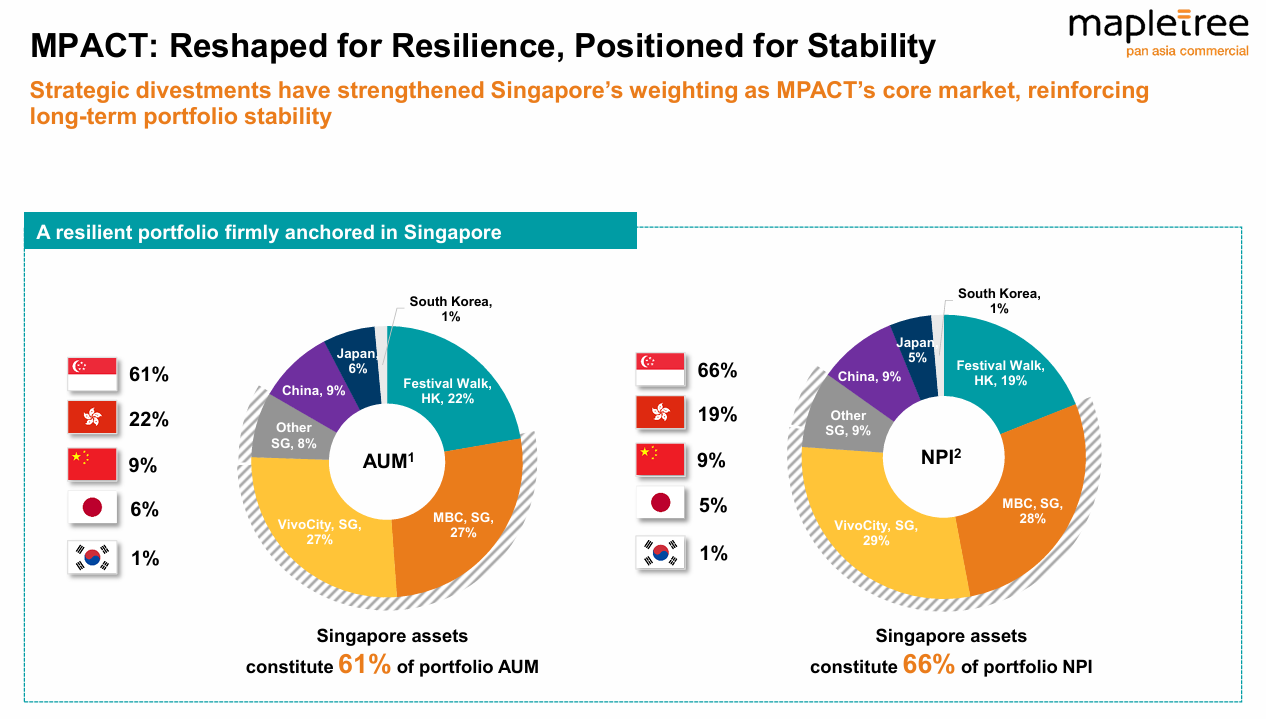

Four years on, as of March 2026, MPACT’s portfolio valuation was around S$15 billion, mainly due to the deterioration of market conditions in overseas markets and a stronger Singapore dollar (which is the reporting currency of the REIT).

Throughout this period, several divestments were also completed to refocus the portfolio on core assets, such as the sale of two properties in Japan as well as the office tower of Festival Walk in Hong Kong. One particular sale transaction in 2024, for Mapletree Anson in Singapore, helped MPACT to reduce its leverage and tide over the high interest rate environment.

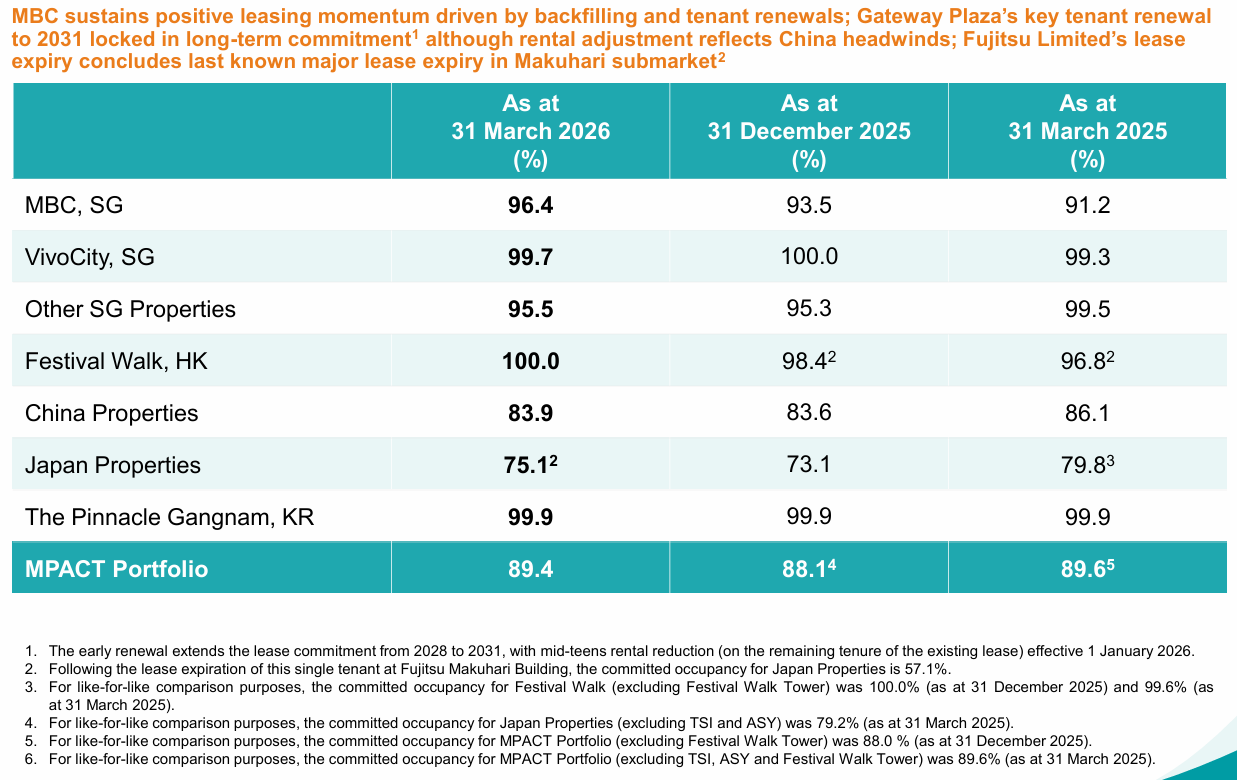

Despite the portfolio reconstitution efforts, operational challenges still plagued MPACT given the persistent rental pressure and vacancy woes in its markets outside Singapore. For one, committed occupancy at its China properties dipped further to 83.9% from 86.1% a year ago.

The concern is greater for Japan, where occupancy will likely have fallen to below 60% after the lease expiry at the Fujitsu Makuhari Building. Leasing will be challenging, as efforts to re-let the converted space as a multi-tenanted building will face the current demand-supply imbalance present in the Makuhari submarket of Chiba prefecture.

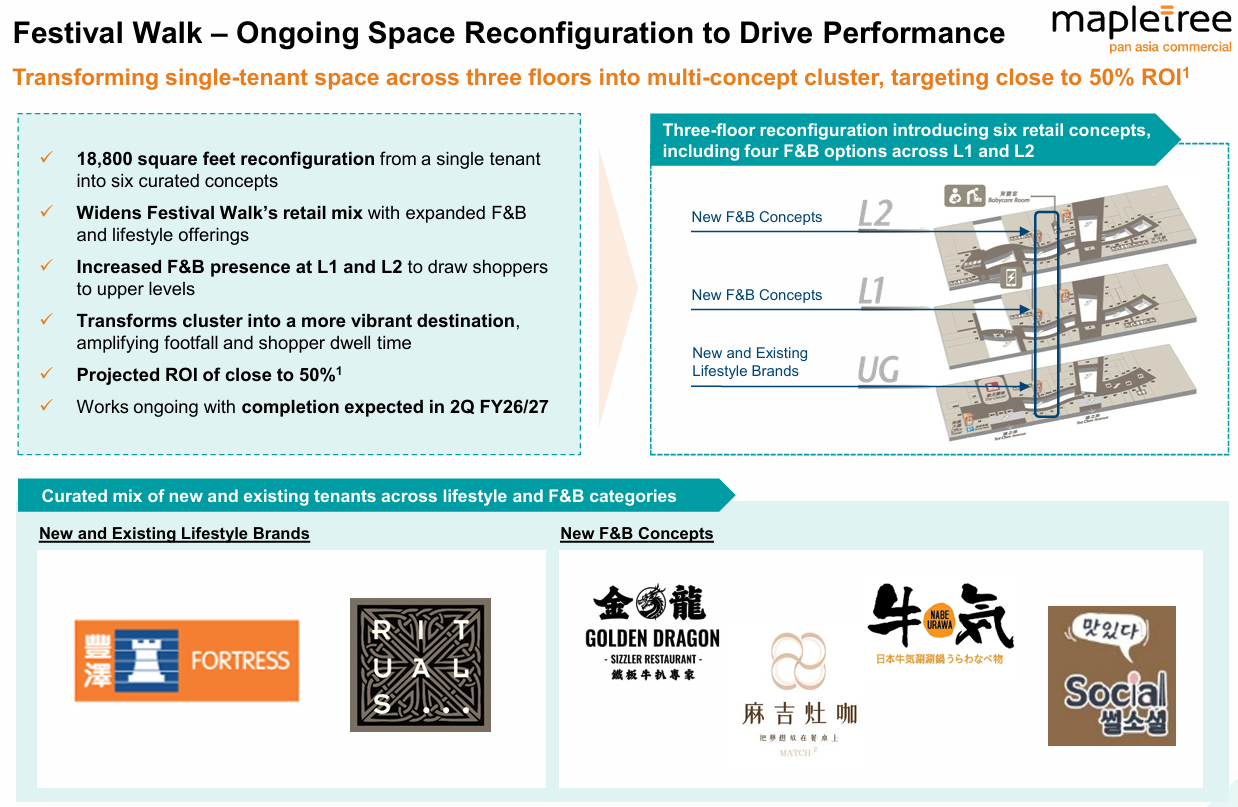

Barring the challenges of the smaller assets, the underperformance of Festival Walk may be a key factor weighing down MPACT. Once a crown jewel retail asset of Mapletree North Asia Commercial Trust, it underpinned the REIT the same way VivoCity did for Mapletree Commercial Trust before the two REITs merged.

However, a series of unrest and macro uncertainties in Hong Kong affected the property’s performance. In the past three years, there was also a trend of Hong Kongers travelling into nearby Shenzhen and Guangzhou for getaway trips, diverting local spending to these neighbouring cities.

As a result, Festival Walk faced difficulties in both lease negotiations and delays in adjusting the tenant mix. A longer-than-expected turnaround of Festival Walk continues to exert rent pressures, especially so for rental reversions as the mall has chosen to defend the occupancy level so far. That said, some early signs of optimism are surfacing in the latest quarter, with foot traffic converting to tenant sales more effectively than 2025.

While markets have been discounting the combined quality of assets within MPACT, the strength of VivoCity in its Singapore home market cannot be refuted. More than being just a resilient mall in Singapore, it is also a key contributor of much-needed growth for the REIT through a virtuous cycle of asset enhancement initiatives and strong rental reversions. The nearby business park asset, Mapletree Business City, also helped anchor the Singapore portfolio with its resilient valuation of S$4 billion.

Not surprisingly, some may hope for MPACT to return to its roots of Singapore-centric core assets faster. But perhaps what is more important for the REIT at this juncture is to carefully manage its timing of potential acquisitions and disposals given the diverging fundamentals of its home market and overseas markets. A mistiming of capital recycling may risk further valuation derating which can take years to recover.