Prada: A new marketing cycle

Commercial investments and retail execution of Prada and Versace will be critical in catalysing the brand momentum necessary to replicate Miu Miu success.

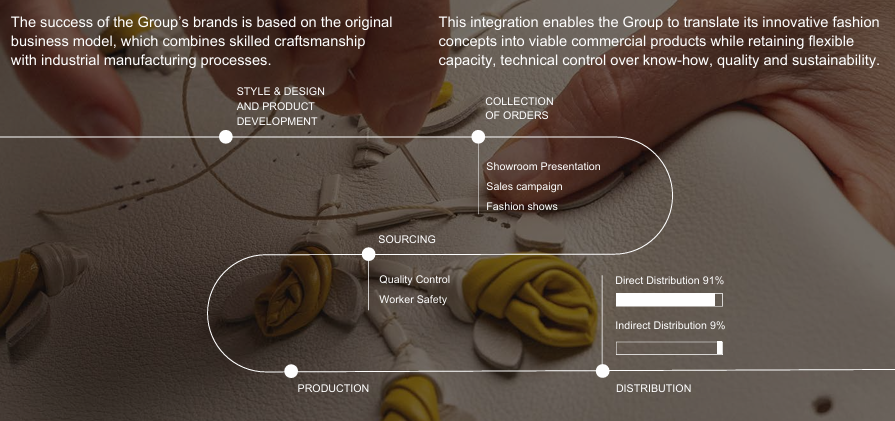

Faced with more than a year of reset in the global luxury industry, brands are navigating a delicate equilibrium: maintaining relevance among an established clientele while capturing a new generation of aspirational consumers. What is consistent across most of the luxury space, from LVMH and Kering to Zegna, is the realisation that brand equity and pricing power must not be compromised even in this downturn. This strategic pivot is characterized by a tightening of wholesale and outlet channels in favor of a disciplined, full-price retail model.

For the first quarter of 2026, Prada Group managed to eke out a small positive growth despite the volatility we have seen coming from geopolitical tensions and waning consumer confidence. With the integration of Versace this year, Prada Group’s portfolio will now be anchored by three main brands each in their own growth cycles. By brand, Prada is still trying to re-engineer a recovery towards growth, while Miu Miu is fighting to keep its strong growth momentum going.

To many in the industry, this is arguably one of the toughest trading environment in recent memory. Coming off multiple years of price hikes, many luxury brands are truly testing the thresholds of their customers’ purchasing intent. By resisting downward adjustments of prices, these brands are essentially prioritizing the defense of their long-term prestige over short-term sales volume. Perhaps rightfully so, it may be harder to elevate a brand’s pricing power back up if they embark on price reductions during a downcycle.

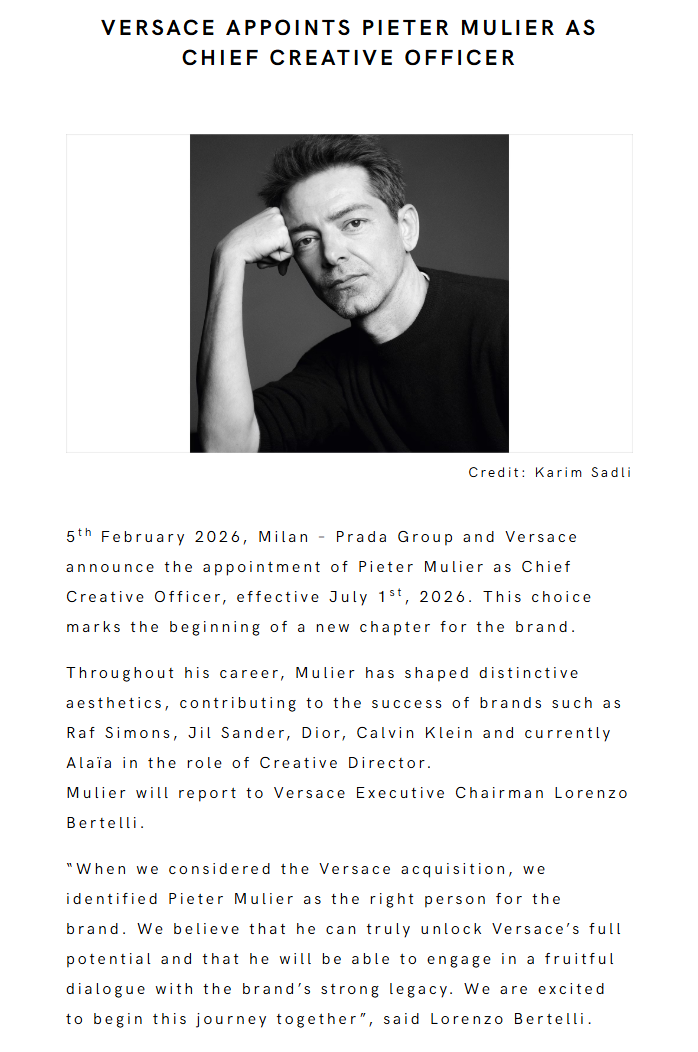

Pertaining to full-price sales, Prada and Versace remain a work-in-progress while Miu Miu is faring much better in terms of pricing power. Operating predominantly through a direct retail model, Prada Group continues to streamline their wholesale distribution channels to maintain better control of their brands. This is especially so for their newly-acquired Versace brand, where the separation from Capri Holdings will progress towards a completion by end of this year, and a debut collection under the new creative direction should come in 2027.

Since its IPO more than a decade ago, Prada Group has already positioned itself to be focused on Asia Pacific. Having chosen to list in Hong Kong instead of Italy, its ambitions remain anchored in the region here, with Asia Pacific (including Japan) making up 46% of their total retail net sales for 2025. Asia is their largest market, followed by Europe at 30%.

Looking ahead, commercial investments into Prada and Versace brands will be critical to catalyst the brand momentum necessary for renewed growth. The company has executed well in the previous cycle, and now it is an opportunity for management to replicate the success of Miu Miu at its other brands. With early signs of green shoots at the core Prada brand, the outlook is turning positive as the revival in consumer interest for Prada is underway. It should, therefore, not come as a surprise if the company is able to continue delivering above-market performance in 2026 while also integrating and repositioning Versace for a fresh 2027.